The current all-time low interest rate environment in Australia is having a profound impact on both the residential and commercial property markets. What may surprise many is that interest rates in Australia have been trending downwards for the past 30 years. With the RBA lowering the official cash rate to 1.50% in August and more rate cuts expected, the term ‘lower for longer’ while being overused, is justified.

The second rate cut in August was a signal from the RBA that there is still some caution around sluggish global growth, low commodity pricing and subdued inflation. The general consensus is that rates will remain at this level with further cuts expected over 2017. So, what does this mean for the property markets?

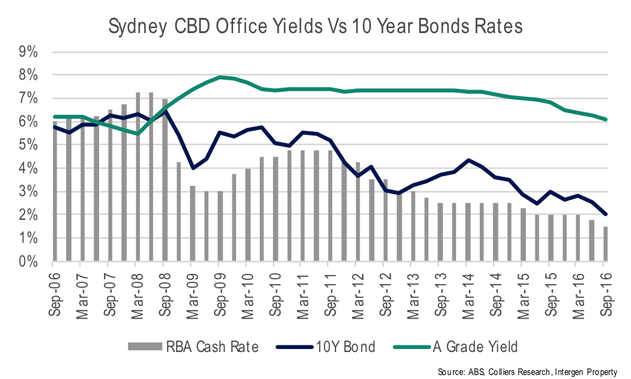

From a commercial property perspective, the ‘Hunt for Yield’ is one of the driving forces behind elevated investment markets. While bond yields and short term interest rates have been falling, prime CBD yields in Australia for example have remained relatively stable. If the spread between historically low real bond yields and yields for office, retail and industrial markets remain high by historical benchmarks (as shown in the graph below), the positive story behind investing in commercial property will continue.

The lower cost of borrowing is also having a structural shift on valuation metrics. Internal rates of return (IRR) are being re-calibrated resulting in lower investment hurdles. The long term implied IRR for Australian prime CBD office assets is currently 7.9%, the lowest in 30 years. In a JLL Asia Pacific survey, evidence suggests that major institutions are currently targeting 7.7% vs. a three-year historical average of 9.6%. Looking forward, the tighter overall returns are expected to remain stable within the property sector for as long as returns from competing investments remain compressed.

While interest rates do play a vital part in influencing markets, property fundamentals such as supply and demand, also have varying impacts on yield movements. It is also worth mentioning that in stages over the last 10 years, yields movements have not always correlated with interest rates as shown from Sep 08 to Sep 09 on the above chart. At this point a yield softening and interest rate contraction was recorded, as markets corrected in the aftermath of the GFC.

Residential markets across Australia, while patchy, continue to experience strong house price growth especially in Sydney and Melbourne with year to date growth figures published by CoreLogic showing an increase of 13.2% and 11.0% respectively. The low interest rate environment has been a precursor for the heightened demand in the sector over the past couple of years with national housing turnover figures remaining strong.

The outperforming housing market has driven pricing to the point where affordability is a big issue for many purchasers. The desire to live close to the major centres (eg. inner Sydney) remains a trend, and therefore investors are changing their thinking of whether they buy or rent, and the type of dwelling that they are willing to live in. Developers have pre-empted this and therefore units and multi-dwelling approvals have risen from 4,162 in July 2006 to 10,284 in July 2016, unlike house approvals which have remained relatively stable around 9,000 per year.

As house prices continue to rise in cities like Sydney and Melbourne, the opportunity to invest is becoming hard to grasp for many buyers, especially for those who are new to the market. This is forcing some individuals/families to overcome their desire to own the traditional ‘house and land’ product and move to smaller units which are within their price bracket. For others, renting is becoming a long term solution. The thought of not having a large mortgage over their head and the flexibility this gives them is an attractive alternative. This is shown by the value of investor loans in June 2016 grew by 3.2% compared to the more modest 1.8% growth in the owner-occupier market.

Despite the risks for the Australian economy, the overall direction for the country is a positive one. With interest rates expected to at least hold for the next 12 months, investors must adapt to the new benchmarks set by the lower interest rate conditions. While the real question is whether these changes are structural or cyclical, we feel that investors who are delaying decisions pending an imminent return to “normal” conditions maybe waiting for a prolonged period.