The retail world has evolved dramatically over the past decade. Technology advancements, mainly through the introduction of online retailing, has allowed consumers to have an almost unlimited access to goods both locally and globally. While this is a positive from a consumers point of view, the saturation of domestic and foreign retailers is allowing consumers to be increasingly fickle. The introduction of global brands has shaken up the industry resulting in a natural attrition of some retailers due to the increase in competition. With our current portfolio having exposure to Large Format Retail (LFR), we thought we would delve into some key themes impacting the LFR space, along with highlighting Intergen Property Group’s (IPG) view on how to keep LFR assets sustainable in a rapidly evolving sector.

Online shopping sent a wave through the retail sector since its introduction in the early 2000’s and has steadily taken a larger proportion of consumer spending over the past 15 or so years. The National Australia Bank (NAB) Online Retail Sales Index released in February 2017, states that the Australian online retail market was worth $21.65 billion in the 12 months to December 2016. This is 10.4% higher than the previous year and 7.1% of total retail bricks and mortar spend.

This rise in online spending has led to e-commerce continuing to influence the offering of the traditional bricks and mortar shopping mall. As online shopping penetration increases, shoppers are focussed on purchasing electronics, books, music, apparel, sporting and outdoor goods. On the other side of the equation, food and beverages, supermarkets, liquor, DIY, gardening, and healthcare tend to be less affected by the change and have out-performed. This has subsequently resulted in centre managers/owners having to reshuffle their tenant mix to stay current with consumer needs and wants.

An essential element to all strong performing retail assets, is the tenant mix. LFR centres have evolved over the years to now incorporate a greater diversified tenant base. This has introduced a high level of competition among retailers and in particular the opportunity to compare prices and products in the one location on the one shopping trip. This trend must continue, especially as competition increases and centres fight for potential customers. The incorporation of non-discretionary tenants that offer goods and services such as food/beverage, medical, childcare and healthcare to drive weekday traffic has been a strategy implemented by several groups and one approach to improve moving annual turnover.

The performance of household goods trade has been solid over the past few years on the back of the strong construction cycle which is partly why the LFR sector has recorded strong leasing demand. This has also had a significant impact on LFR investment yields, with JLL research’s midpoint yield compressing 100 basis points over the year to December 2016, shifting to 6.5%. While a slowdown in residential construction has been well documented over the past 12 months, underlying population growth (1.6% forecast over the next 5 years) across Australia will continue to bolster new supply over the foreseeable future. So, while a select part of the retail sector will continue to be impacted by online retail, we at IPG believe that the underlying LFR drivers are sustainable and likely to aid the sector moving forward. While this is a key consideration, a ‘sustainable’ asset must also have sound property fundamentals such as prime location, good quality improvements, solid tenant mix and covenant.

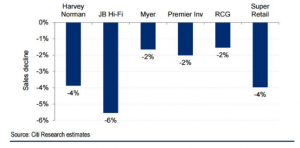

With the announcement that giant online retailer Amazon is hitting Australian shores in mid to late 2017, many major brands in Australia are speculating on the full impact this will have on the industry. Experts believe that Amazon could generate sales of up to $4 billion in Australia, which will have a substantial impact on several industry sectors. While Amazon’s impact on retailers will be varied, we expect the greatest impact to be recorded by electronic retailers given the range of products Amazon offer. Citi Research believes Amazon could capture 7% of electrical goods market based on its success in the UK and US.

Potential Sales Impact from Amazon’s Entry

With regards to the LFR space, the entry of Amazon will no doubt have an impact on the sector. However, business owners who are creative and embrace the capability of new technology will enable their stores to be more sustainable and profitable moving forward. ‘Click and Collect’ is already in use and an example of a simple but effective retailing solution. Does a customer value free home delivery if they have to stay at home for that three hour shipping window? ‘Click and collect’ allows the consumer to pick up their goods when they please. This is one example of many new systems in place that allow flexibility and greater options when purchasing goods online.

Because there is a constant threat to the retail world through online retailing, the entry of global brands and creative new consumer platforms, all retail categories including the LFR space must continue to develop strategies to anticipate the continually evolving nature of the retail landscape.

Failing to recognise these risks will see the performance of their assets decline and vacancy within the centre to increase. IPG believes the key to remaining current in an evolving retail world is to embrace technological change, strive to dominant your catchment, think strategically about your tenant mix and be creative about how your centre can gain competitive advantage over neighbouring centres in your trade area.